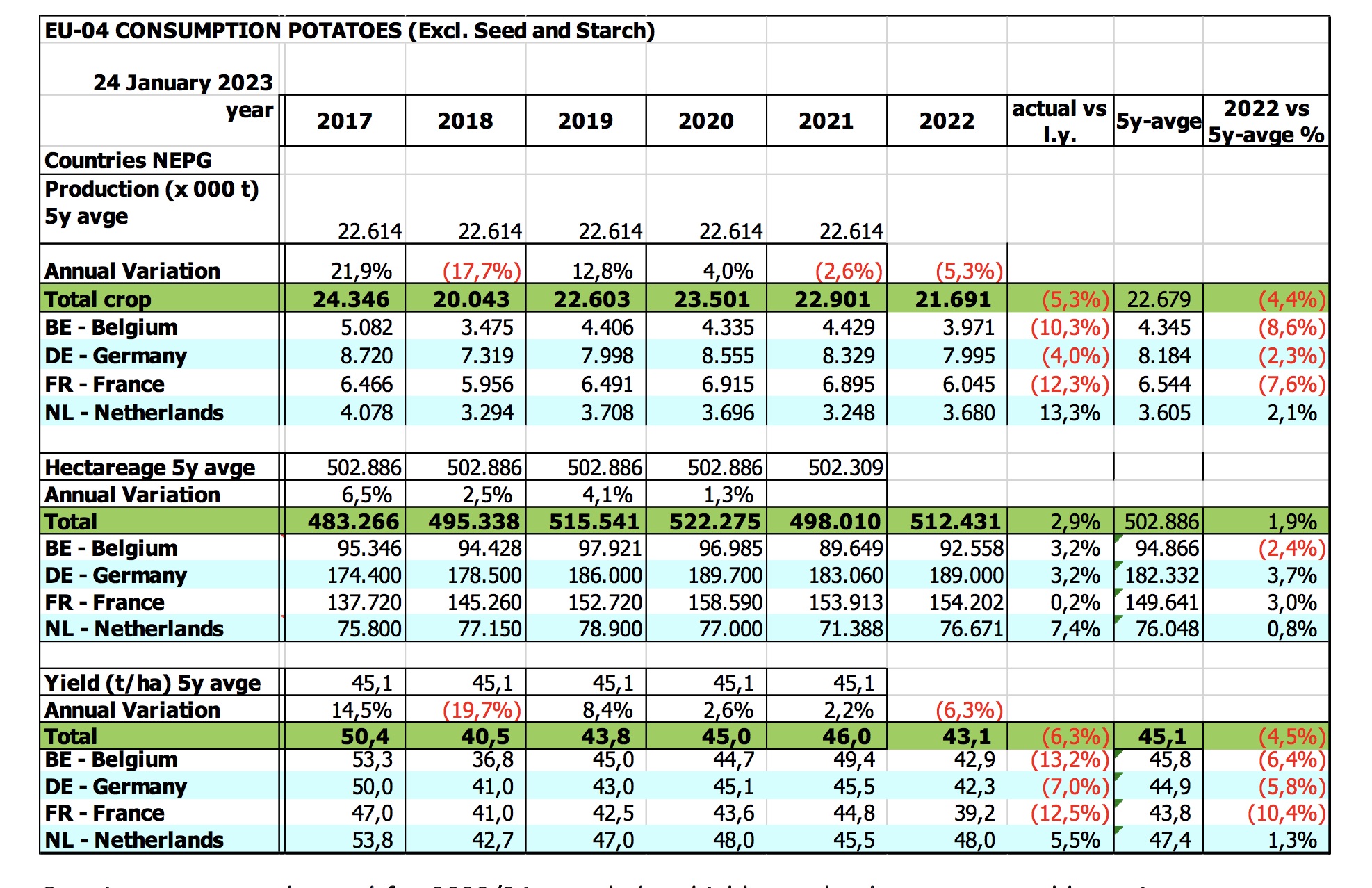

Lower potato production throughout Belgium, the Netherlands, France and Germany and little effect of inflation, has up to now resulted in reasonably good free market prices for producers, reported the North-western European Growers (NEPG) association on January 24. Higher contract prices and additional risks to farmers have already led and will lead to different consequences for the whole potato sector – from seed growers to retailers and consumers. Final area, yield and production figures show that in spite of 2.9% more hectares under cultivation compared to last year (512,400, or + 14.421)), a lower yield per hectare of -6,3% led to a total crop output harvest of 21.69 million tons (-5.3 %; ie a reduction of 1.2 million tons).

Demand for potatoes is good, with processing plants throughout North-western Europe eager to buy spuds at a time when factories are operating at full capacity.

New or modernized processing units and new factories (those that have recently come on line or will be activated soon) have led to historical high contract prices which have gone up by 30% to 45%. Processors in Belgium, France, Germany and the Netherlands are eager to receive more raw material during the rest of the ongoing season and the 2023-24 campaign.

New or modernized processing units and new factories (those that have recently come on line or will be activated soon) have led to historical high contract prices which have gone up by 30% to 45%. Processors in Belgium, France, Germany and the Netherlands are eager to receive more raw material during the rest of the ongoing season and the 2023-24 campaign.

These higher contracts should cover the very much higher production costs and inflation that growers are facing now, and ensure a continued attractiveness for supply potatoes to further processors, who will need at least 500,000 tons more during the 2023-24 season.

Risks facing growers are ever more important and force majeure is not always mentioned or included in contracts.

“Global warming, the rise of environmental constraints and the structure of potato cultivation on rented land on an annual basis renders potato production more risky and difficult,” according to an NEPG press release issued on January 27.

Facts and figures previously posted by the association show that yields per hectare have been going down during the last 10 years. The main factor leading to reduced yields are shifts in weather patterns, but in some cases it is also a combination of problems linked to the soil (compaction, less organic matter content, nematodes, too short rotations…). This is an issue which has to be faced by the whole potato chain.

Genetics [most breeders are very active producing new robust varieties, i.e. tolerant/ resistant to blight, more tolerant to abiotic stresses and/or needing less nitrogen (but also resistances to nematodes, Virus Y…)] and new/adapted cropping techniques are the main solutions. The use of NBT (New Breeding Techniques) could also help.

NEPG estimates that at least one-third of potatoes harvested in its zone are grown on rented land on an annual basis. “This does not always help farmers adapt their cropping techniques, but does also lead to the fact that part of the additional value goes directly into the pockets of lessors or land renters who take zero risk,” according to a press release from the association.

Risks are multiple and, on the increase, compared to 10 or 20 years ago. Due to fluctuating productions and free buy prices, and to a lesser extent changing contract prices, farmers now have to include a series of “new” risks to manage. These include climate change, geopolitical (i.e. the war in Ukraine) and health events (ie the Covid 19 pandemic), access to water, tighter EU regulations regarding fertilizer (mainly nitrogen, be it farm-sourced or mineral) and pesticide uses. On top of that, contracts are more different (between processors) and more difficult to fully understand than before.

Finally, risks are usually (or could be) partly covered by insurance policies. Relatively simple “hail and storm” insurances are now also more complicated and expensive, as they have to cover drought, excessive heat, flooding, erosion, mudflows etc.

Higher contract prices could stimulate greater potato hectareage cultivation as well as bigger contracted potato volumes.

Seed growers, starch potato growers and table potato producers could partly switch from their current production to produce tubers for chips and crisps.

These developments could lead to profound imbalances throughout the whole of the potato sector.

Seed production costs have risen and there is no indication that buyers will increase the price they pay for seed. This could lead to less seed production during the 2023 season. The seed sector could lose at least 5,000 hectares, which would lead to shortages and higher prices for consumption growers in spring 2024. “Here also, the problem has to be dealt with by the sector and not only by seed and consumption growers,” concluded the NEPG.