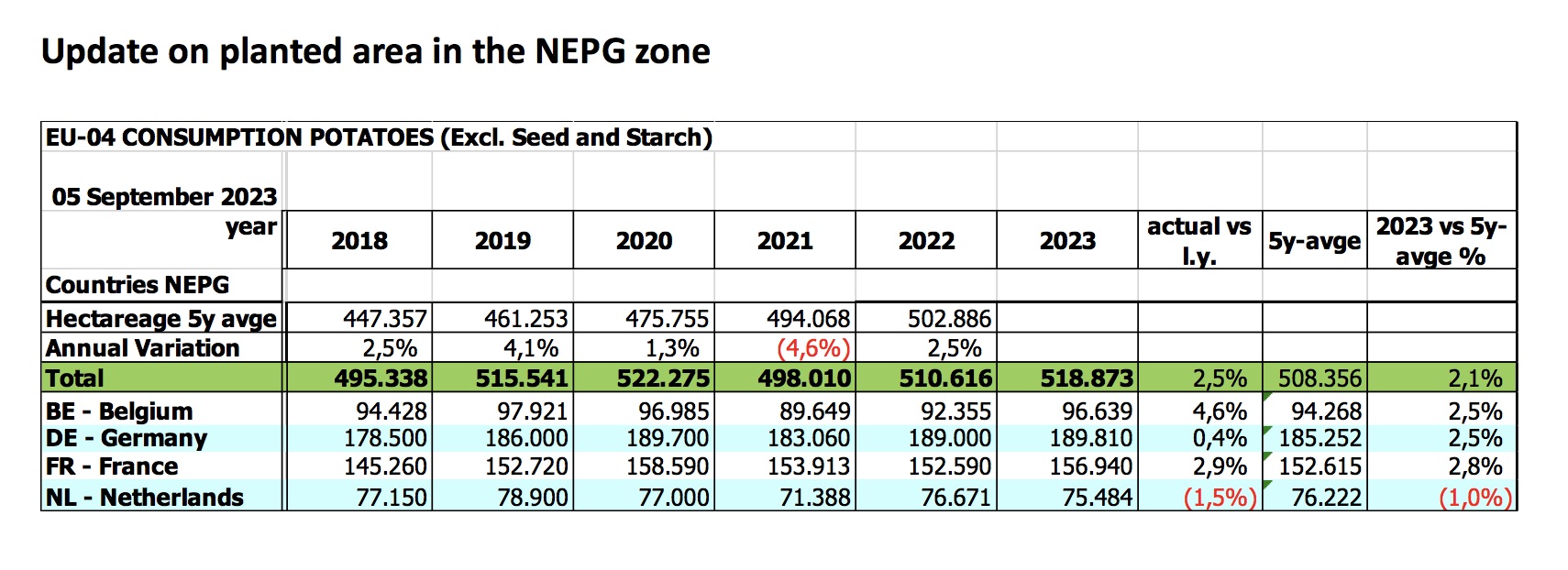

In spite of challenging weather conditions during the past four months, potato production yield estimates from the North-western European Potato Growers (NEPG) suggest a return to multi-year averages. The association estimates that farmers will harvest approximately 23 million tons of early and main crop potatoes. This is 1.3 million tons more than in 2022 and equal to 2021 production.

Average planting dates were generally three weeks later than usual in Belgium, Germany, France and the Netherlands (around May 15-20 instead of April 20-25). While the region’s weather in August led to a sharp increase in yields, there were also very high levels of late blight (Phytophthora infestans).

Planters of Mid-late Fontane and Challenger varieties, and the late Markies potato variety will not benefit from a full schedule of growing days, unless crops are left in the ground until mid-October. Lower tuber counts and physiological disorders (hollow heart, misshaped, rot) and above all tuber blight will impact net production. In addition, mitigated under water weights will lessen processing yields.

Tuber Blight Assessment Urgent

Growers have been strongly encouraged by the NEPG to check every cultivated field to conduct through tuber blight evaluations. Assessing the impact is of utmost importance to decide on further steps to take regarding haulm destruction and storage planning. The association stresses the importance for producers to communicate on this issue with their buyers. Weather in the coming weeks will either stabilize the problems (blight, hollow hearts, rots) or sharpen them.

Higher Processing Needs and Good Export Prospects

Whereas production in 2023 may be compared with output in 2021, processing needs have risen significantly. Value-added potato producers throughout the NEPG zone need at least an additional 2,000,000 tons of raw material compared to two years ago, Following lower output in Poland and Southern Europe (due to smaller planted area and unfavorable weather conditions) the export season has already started and competiton between industrial and export buyers will again be on the agenda. Market experts have optimistically assessed that the demand for processed products in Europe will continue to grow by around 4% every year.