Harvested potatoes from farms in Belgium, Germany, France and the Netherlands weighed in at 24.7 million tons in 2024, a 6.9% rise over the previous year. Despite the supply increase, reports the North-western European Potato Growers (NEPG) association, the market remains dynamic.

Producer prices rose from €12.50 per 100 kg during the October to November period to €30.00 at the beginning of February. The rapid rise since the beginning of January is rather surprising. Stock assessments over the coming months, as well as the timing and conditions of spring planting, will be of prime importance for price trends this season.

2025: Area Increase with Weak Profitability risk?

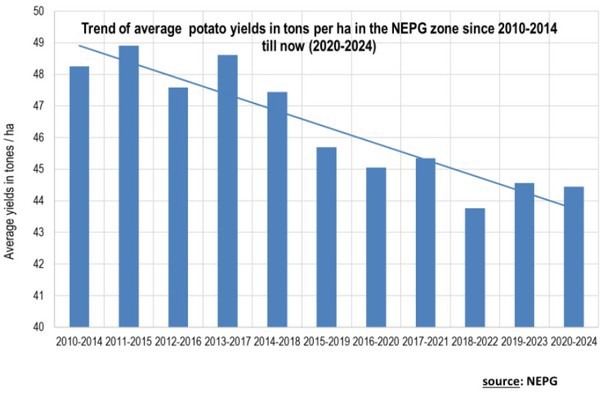

With a dynamic market (and little other alternatives), the NEPG believes that this coming spring it is very likely that farmers will plant more potatoes than last season. Growers must seriously take into account the yearly trend of lower yields (see graph below), which mean higher production costs per hectare. But a higher area of cultivation means higher risks of a good overall production should early planting be followed by a normal growing season.

Stable Contract Prices and Higher Production Costs

While seed is usually less expensive than last spring (Innovator type varieties are the exception), they are up by 10% to 15% when compared to 2023 prices. Production costs have risen somewhat, and risks are ever more important for farmers. Some processors use dissuasive tariffs to encourage growers to limit soil tare.

Throughout the NEPG zone, contracts are mostly stable throughout the storing season. Future changes and evolution will depend on free buy prices for processing potatoes.

Uncertain World Markets and Export Challenges

Today’s market is influenced by more risks and costs in line with potential trade policy changes in the United States, expanding Chinese and Indian experts of frozen fries and tougher environmental regulations in the EU.

EU-04 export of frozen potato products could suffer from future higher tariffs in the USA. At the same time, the European potato sector must be aware of growing alternative fry export players in Egypt, Argentina and Turkey, as well as in China and India.

Meanwhile, the economic impact of climate change policies, tougher pesticide regulations and availability, more soil borne problems (nematodes, wireworm, edible nutsedge…) and diseases such as Stolbur as well as more problems and legislation linked to nitrogen leaches in ground water make potatoes technically and economically more difficult to produce and financially more risky.

Uncertainties abound concerning the coming season’s free buy prices and processed products sales. With the very probable bigger potato area and uncertain export markets for the EU-04, growers must be aware they are taking risks in expanding their potato hectareage. Producers must follow processing needs and not precede them.

![]()